The International Consortium of Investigative Journalists (ICIJ) has exposed yet another disturbing layer of crypto opacity in its investigation “Hunt for missing millions unmasks one crypto exchange hidden inside another.” The findings reveal a marketplace built on offshore shells, nested operations, and regulatory blind spots — an environment where victims lose millions, while the mechanisms meant to help them recover funds often produce more legal invoices than restitution.

FinTelegram has covered these structures for years. And once again, as litigations begin — this time led by Dutch fund-recovery specialist Marius Hupkes — we must ask the uncomfortable but necessary question:

Will victims actually see their money again? Or are they simply feeding another system where only the lawyers win?

Nested exchanges, offshore shells, and legal labyrinths

The ICIJ report lays out a clear pattern:

- Kyrrex, promoted as a regulated EU-friendly crypto platform, quietly routed customer activity through its St Vincent offshore entity, which in turn operated “inside” HTX (Huobi).

- Victim funds — including the US$1.5 million savings of a Dutch model — flowed directly from fraud schemes into Kyrrex-branded wallets hosted on HTX.

- Blockchain analytics traced billions through these wallets between 2022 and 2025.

- Regulators retreated behind jurisdictional firewalls. Malta pointed to St Vincent; St Vincent pointed to nobody. Kyrrex itself claimed it had no way to know fraudulent actors were using its platform.

This structure is not an accident. It is a design feature, optimised for deniability and profit. And it leads to the next problem.

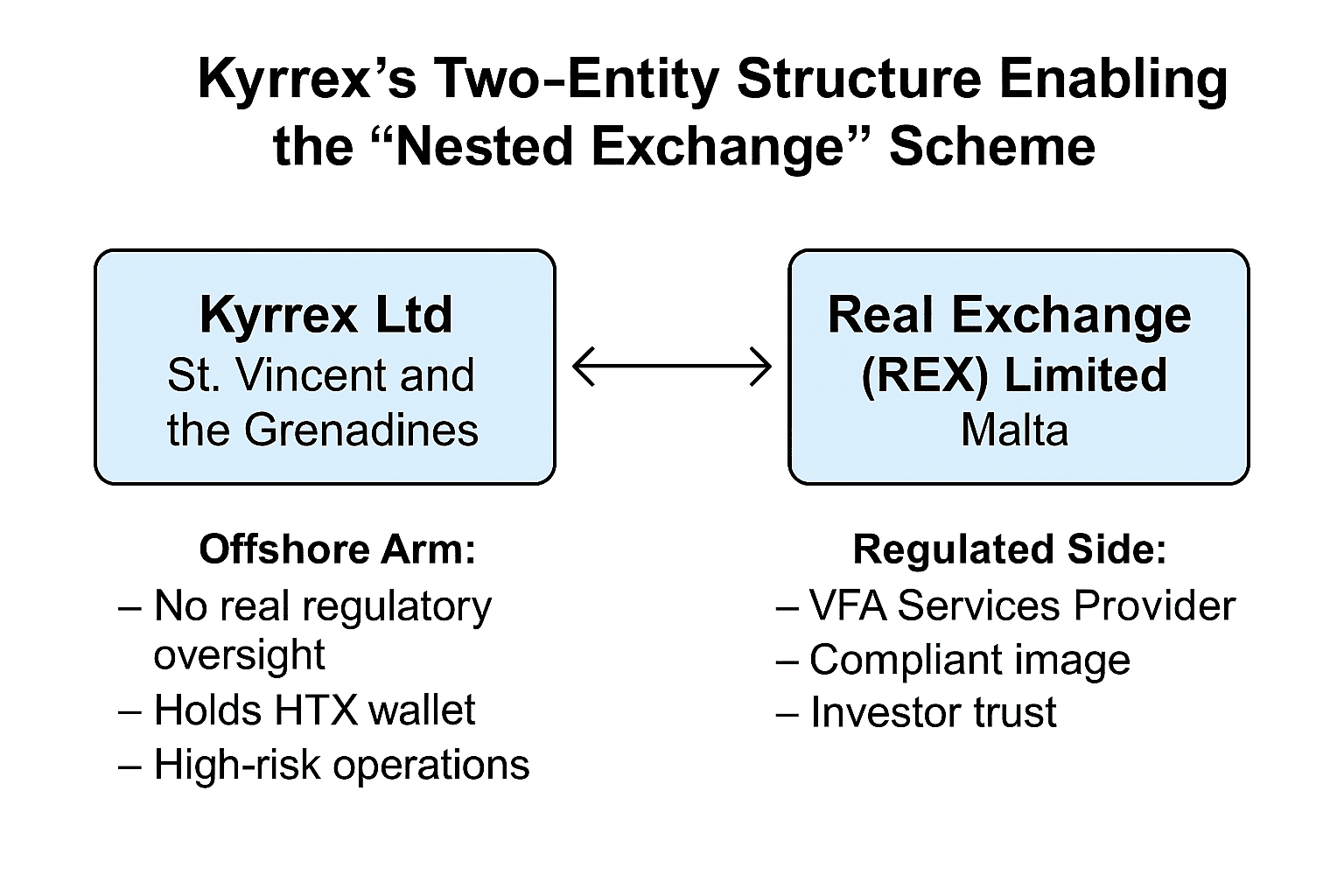

Explainer: How Kyrrex’s Two-Entity Structure Enabled the “Nested Exchange” Scheme

To understand the ICIJ revelations, it is essential to grasp how Kyrrex is structured. The group operates through two sister companies that play very different roles — a classic setup we have seen in many high-risk crypto operations.

1. Kyrrex Ltd — St. Vincent and the Grenadines (SVG)

This is the offshore arm of the operation.

- No real regulatory oversight

- Can open and control crypto wallets freely

- Can interact with unregulated or controversial exchanges

- Can process large flows without meaningful compliance checks

According to the ICIJ investigation, the HTX wallet receiving victim deposits and billions in transaction volume was held by this SVG entity.

2. Real Exchange (REX) Limited — Malta

This entity is marketed as the “regulated side” of Kyrrex.

- Registered under Malta’s Virtual Financial Assets (VFA) regime

- Used to promote a compliant and EU-friendly image

- But legally separate from the SVG entity

- And crucially: the Maltese regulator does not supervise or take responsibility for the SVG company’s actions.

3. Why this matters

The structure works like this:

Offshore (SVG) does the risky business

— hosting wallets at HTX

— receiving flows linked to fraud

— running high-risk operations that EU regulators would never approve

Onshore (Malta) provides legitimacy

— regulated façade

— EU marketing

— investor trust

— a shield against scrutiny (“that entity is not ours”)

4. The outcome for victims

Victims see “Kyrrex” and assume one company, one jurisdiction, one responsible party.

The reality is:

- The wallet belongs to the SVG entity

- The brand belongs to the Maltese entity

- The victims are caught in between

- And the regulators disclaim responsibility

This legal and operational split is precisely what makes enforcement, litigation, and recovery so difficult — and why expectations must remain cautious.

Litigation begins — but will it produce anything beyond paperwork?

Victims, understandably desperate, are turning to legal action. Dutch lawyer Marius Hupkes has filed claims arguing Kyrrex bears responsibility for failing to prevent fraudsters from using its exchange infrastructure.

Hupkes is experienced, reputable, and does not take frivolous cases.

But here is the uncomfortable reality FinTelegram must highlight:

Winning a lawsuit against an offshore crypto shell does not equal real recovery.

We have seen this pattern countless times:

- You win the case.

- You get a nice judgment.

- The defendant has no accessible assets in the jurisdiction where the judgment applies.

- Enforcement becomes a multi-year chase across legal deserts.

- Meanwhile, the lawyer’s fees must be paid — reliably and in full.

Victims often convince themselves they are part of a “collective effort” with high odds of success. But the actual risk-reward ratio looks more like this:

Victim risk: high

Victim cost: high

Victim recovery: uncertain, often negligible

Lawyer’s outcome: fee secured whether recovery occurs or not

This does not make the lawyers malicious — it makes the system misaligned.

The deeper issue: Offshore entities can always disappear

Until recently, Kyrrex operated through a dual-channel model — a global platform at kyrrex.com/global and an EU-branded platform at kyrrex.com/eu — a structure long familiar from earlier binary-options and CFD schemes. Web-archive records show that until early 2025 the operator of kyrrex.com was Kyrrex Limited (SVG), with no mention of Malta-based Real Exchange (REX) Limited. REX, in fact, operated only kyrrex.mt and later kyrrex.com/eu, and has appeared as the operator of kyrrex.com only in recent weeks.

At the start of 2025, yet another entity — Kyrrex Operations LLC (a US company registered with FinCEN as MSB #310024013725) — briefly appeared as the website operator. As of November 2025, the “global” portal kyrrex.com/global has vanished, Kyrrex Limited (SVG) has disappeared, and only kyrrex.com and kyrrex.com/eu remain.

Such shifting operators, disappearing entities, and inconsistent domain governance provide a poor foundation for any legal action seeking accountability or fund recovery. Even if Hupkes secures a legal victory:

- The relevant Kyrrex entity sits in St Vincent.

- Its operational infrastructure is intertwined with HTX, an exchange with a long record of regulatory controversies.

- Funds have been commingled, mixed, moved, laundered or dissipated months or years ago.

- No early asset freeze was executed — the single biggest prerequisite for successful recovery.

This leads to the most critical point:

The money is almost certainly gone — long gone — no matter what the courtroom decides.

And offshore entities know this.

Their entire model relies on legal distance, fragmented jurisdictions, and regulators shrugging responsibility.

The question nobody wants to ask: Who really benefits from this litigation?

From years of FinTelegram investigations, a consistent truth emerges:

In cross-border crypto fraud litigation, lawyers almost always recover more than the victims.

Victims, already emotionally and financially drained, often believe litigation is the last hope. But hope is not a strategy. Before joining group lawsuits, victims should ask:

- Which Kyrrex entity is actually being sued?

- Where does it hold enforceable assets — if any?

- What is the fee structure?

- Are there caps on costs, or can fees exceed recovery?

- What is the enforcement pathway against an offshore company intentionally structured for evasion?

- What are the realistic odds of recovering even 10% of losses after costs?

These answers will likely be sobering.

Conclusion: Justice is important — but false hope is dangerous

The ICIJ report is essential reading. It highlights a system engineered to exploit jurisdictional gaps while maintaining a thin veneer of legitimacy. But when it comes to fund recovery, victims must remain brutally realistic:

- Litigation may establish guilt — not restitution.

- Offshore crypto firms do not pay simply because a court tells them to.

- Legal costs can erase the tiny chance of recovery.

FinTelegram’s position remains consistent:

Victims deserve justice, not illusions.

And before committing to expensive, uncertain litigation, they deserve full transparency about the true odds of meaningful financial recovery.

We will continue tracking the Dutch case, Kyrrex, and HTX — and we invite whistleblowers, insiders, and affected victims to share relevant materials confidentially via Whistle42.com.

Only through transparency and data — not wishful legal thinking — can the crypto crime ecosystem be dismantled.

{kind=link}